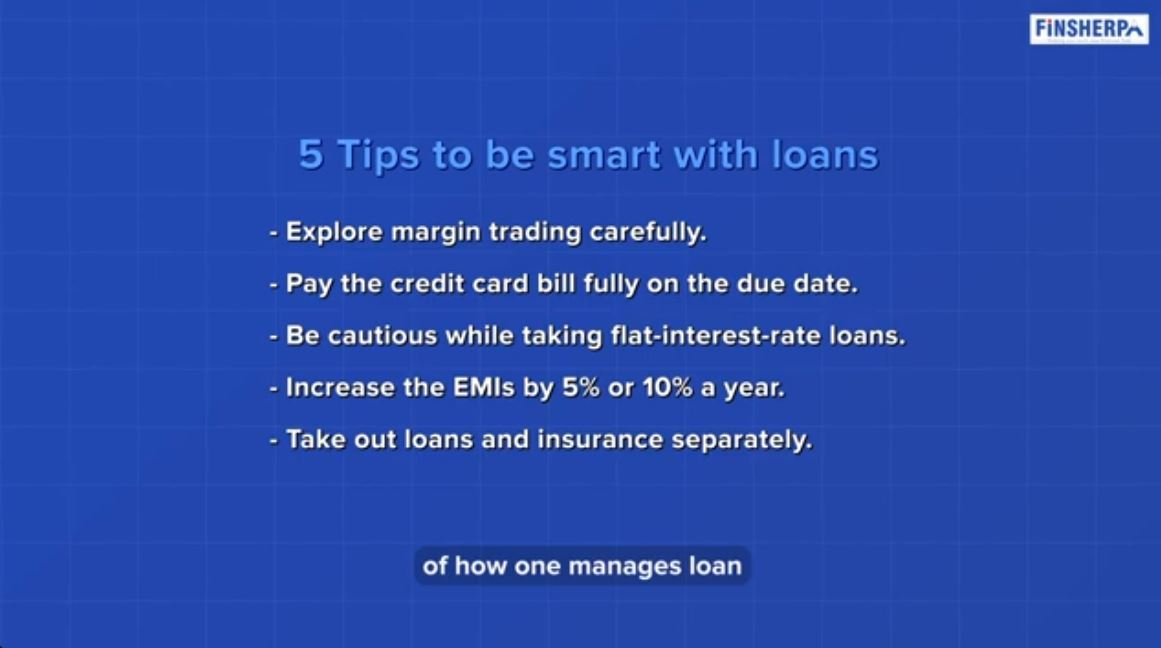

5 Tips to Improve Loan Management and Reduce Financial Stress

Posted By: Blog

Let's explore five tips for managing your loans wisely. Loans are a common necessity for many of us when purchasing assets. However, it's crucial to regularly review and analyze your loans to ensure financial smartness. Remember, saving money is just as important as earning it.

1. Explore Margin Trading Carefully

One common mistake to avoid is engaging in Margin trading. When you invest an upfront amount, such as 15 or 20% of the money, the broker will provide support for you to purchase the entire value of the portfolio or stock. As a result, you can take advantage of the appreciation and benefit from it. With the broker holding the stock, this loan comes with an interest rate ranging from 10 to 12%. Its main objective is to capitalize on short-term profit opportunities.

However, it is important to note that this investment is exceptionally risky and extremely uncertain. There have been instances where individuals engaging in high-frequency transactions realized later that their margin had vanished, causing a loss of 15 or 20% and ultimately reducing their investment to zero.

Reports suggest that 98% of individuals involved in stock market trading do not see returns and ultimately lose money. It is important to approach margin trading cautiously and only pursue it if it aligns with your investment strategy.

Check out the video link for a more in-depth understanding

2. Pay Credit Card Bills Right On Time

Have you ever taken a close look at your credit card statement? It reveals the amount you owe the credit card company for your expenses over the last month. However, it will also indicate that the payment amount is significantly reduced. By saving on your credit card expenses, you managed to save ₹15,000 last month. The system suggests that paying ₹1,250 is sufficient. Consequently, some individuals believe it is wise to pay only 1250 and utilize the remaining credit for an extended duration.

Regrettably, it is the most detrimental action you can take in terms of your wealth. I say this because the interest rate on credit card loans is the highest you will find anywhere. At one point, the company I bank with had a credit card loan rate of 42% per year, which is equivalent to 3.5% per month. Therefore, if you spend $15,000 and make a payment of $1,250, the remaining balance of $13,750 will accumulate interest at a rate of 3.5% for the next 30 days. This cycle will continue until you have fully repaid the entire amount, which is an incredibly large sum.

We don't make that kind of return even in the stock market. This is the most damaging thing for your wealth, so I strongly recommend you pay close attention to it. Therefore, when you use your credit card, always remember to pay off the full amount by the due date, without carrying over any balance. Trust me, this will greatly improve your money management skills.

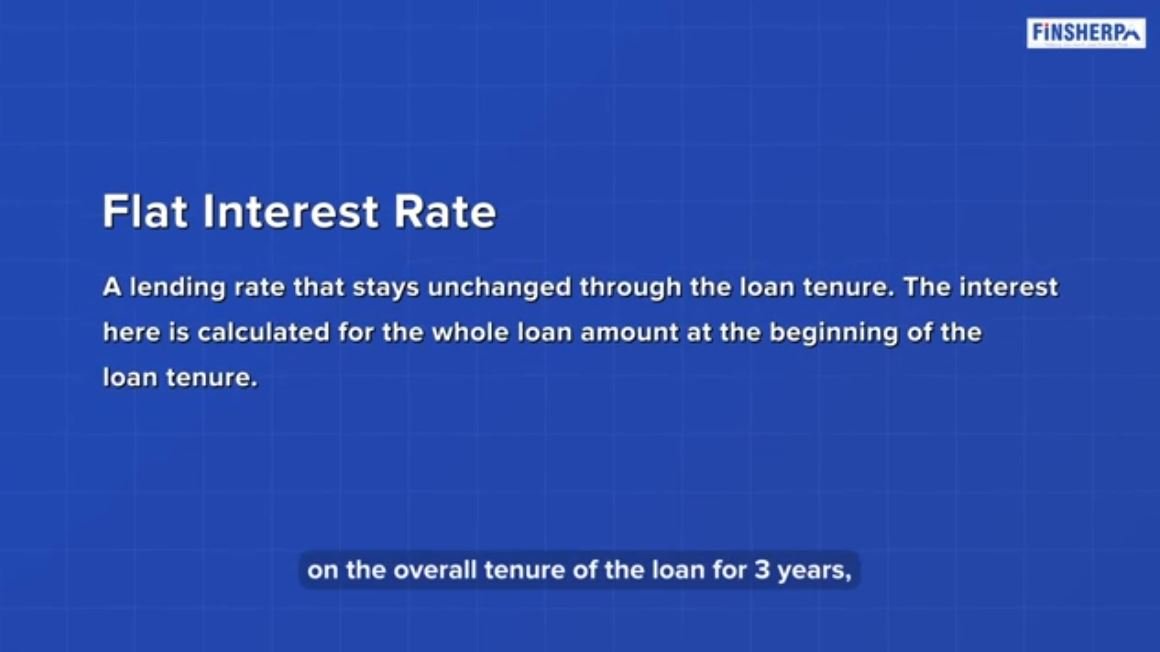

3. Be Cautious While Taking Flat Interest Rate Loans

I received a call from a client who excitedly shared, "Babu, you won't believe it! My banker is offering me a flat rate overdraft of ten lakhs at 9%." Impressed, I responded, "That's amazing! 9% is a very competitive rate for an unsecured loan."

He has decided against applying for a housing loan. There is no collateral involved. It's an unsecured loan with no security, with an interest rate of 9%. This got me curious, so I requested the person to gather more information. According to him, the banker informed him that it's a fixed interest rate of 9% for 3 years.

That's when I found the solution. A flat 9% and 9% on a reducing balance basis are quite different. On a reducing balance basis, the 9% remains constant throughout the loan period. Conversely, a flat 9% means that you have to pay 9% over the entire three-year loan tenure, while your EMIs gradually reduce your outstanding balance starting from the next month.

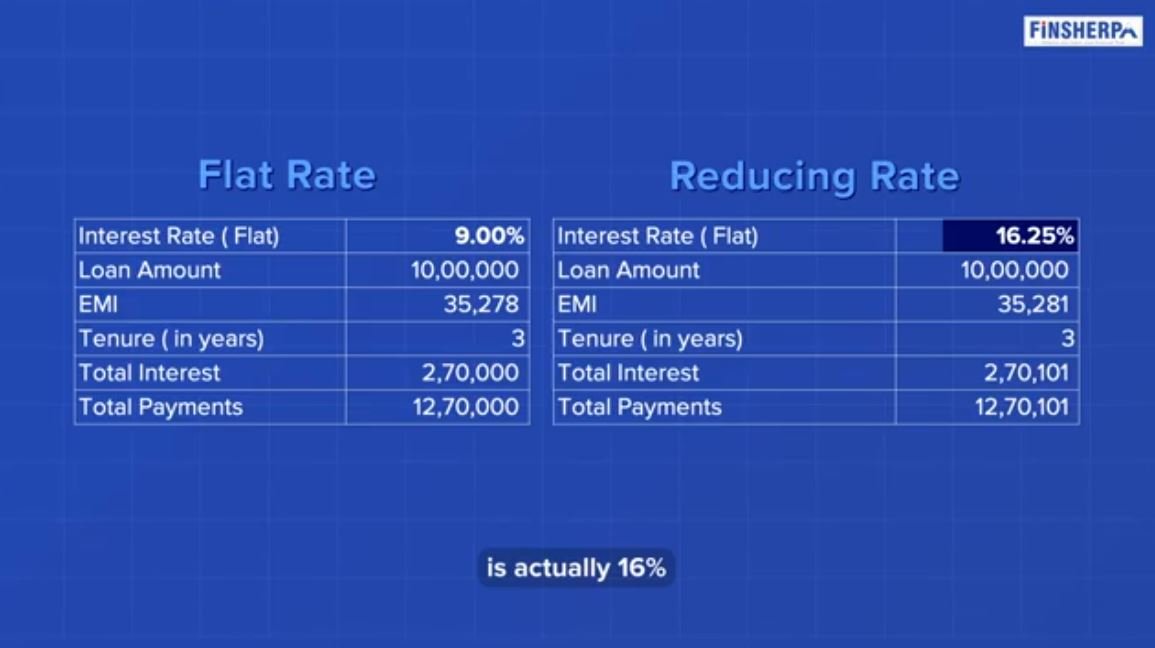

The effective rate for a three-year 9% loan is 16% in this gentleman's case. Additionally, there is a transaction fee of 1%. This means that the transaction fees are collected upfront, resulting in ₹10,000 being collected on a 10 lakhs portfolio. As a result, the gentleman will only receive 990,000, and he will need to pay an additional amount.

It's important to exercise caution when dealing with loans of this kind. The interest rate can rise significantly, and you may also be asked to make two upfront payments. Consequently, the total cost of the loan could exceed 20%, despite the initial impression of it being a cheap loan at 9%.

Check out the video link for a more in-depth understanding

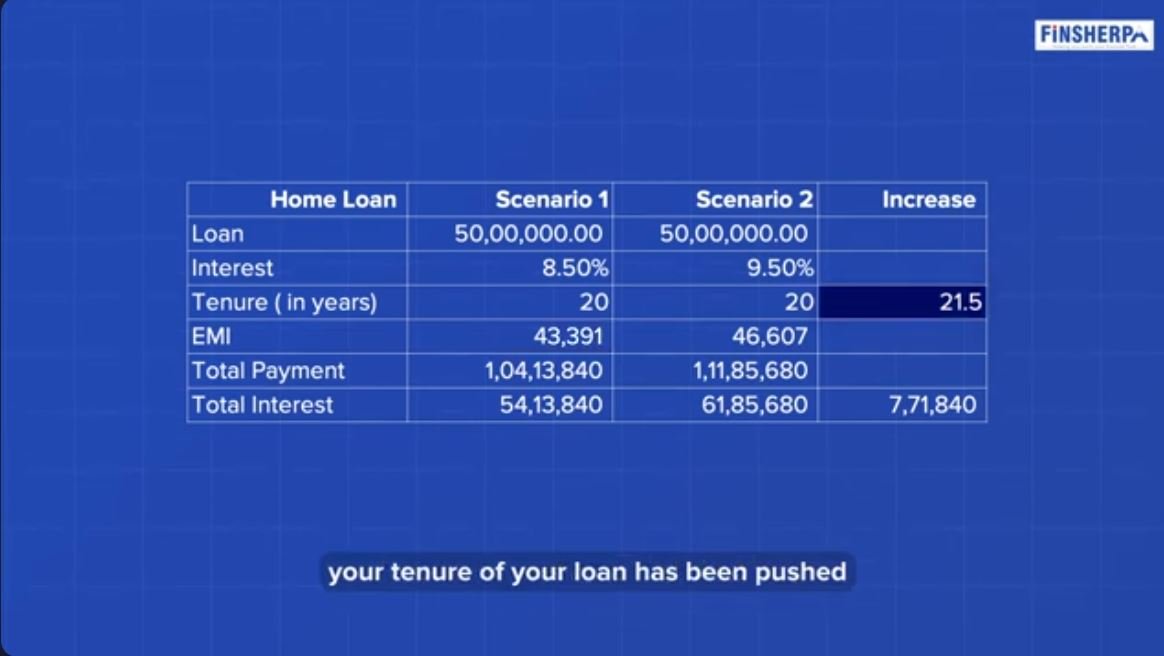

4. Increase the EMI By 5-10% per year on Home Loan

The interest rates for housing loans have been rising steeply, and it appears that most people and banks have not taken the necessary steps to adjust their EMIs. However, this is where the crucial detail comes into play. Every housing loan has a factor that requires the EMI to increase in line with the rising interest rates. If the EMI remains unchanged, the loan tenure automatically adjusts without your awareness. This is extremely important. During such times, it is essential to contact your banker and ascertain your current loan tenure.

Make sure to verify if your EMI hasn't been increased, your loan tenure may have been extended by two or three years. You might have thought it would end in five or seven years, but it could now be ten years. Double-check this information. But if you belong to the category of smarter individuals who have allowed their EMI to rise in tandem, your timeframe remains unaffected. This is another way in which people fail to make wise financial decisions.

Generally, salaried individuals receive a 5 to 10% salary hike every year. Your EMI will rise every year, so it's important to keep your banker informed annually. For example, if you started with a 50,000 EMI and received a salary increase after 12 months, your EMI could increase by 5% or 10%. With a 10% annual increase in EMI on a 20-year loan, you could pay off the entire loan in just 10 years, saving a substantial amount. Make sure to revisit your banker each year to capitalize on your increased income and unchanged expenses. Use this surplus wisely.

5. Take Out Loans and Insurance separately

During my conversation with an investor, I noticed that he had recently acquired life insurance and health insurance. I inquired about the reason behind his decision, as I believed he already had sufficient coverage. To my surprise, he explained that it was a requirement for his loan documentation. The banker had insisted that both his life insurance and health insurance should cover the loan.

Even though the loan only had a 9% interest rate, the unwanted insurance risks caused a significant increase in the overall cost of borrowing. I questioned whether he had explored other banks and institutions offering the same rate without bundling insurance opportunities. He was unable to respond. It is commonly assumed that banks mandate insurance for home loans, but this is not always true. If you already have sufficient life and health insurance, you can present this to your banker and request a loan without the obligation to purchase additional insurance.

Bankers often combine these products out of necessity, but it's wise to distinguish between them. If you're interested in a loan, focus on that alone. As for insurance, if you're already well-covered, there's no need to worry about it. I believe these are five key points to consider when handling a loan, and managing it wisely will surely bring great benefits in the long run.

For the complete video experience, click on this link

Category Finsherpa | Tags